The European equity crowdfunding market will raise €280 million in 2025 through 354 public equity campaigns, involving over 68,500 investors. The figure marks a 12.2% increase compared to 2024 and confirms the progressive consolidation of crowdfunding as a structural channel for financing start-ups and SMEs, two years after the entry into force in all EU states of the European ECSP Regulation, which gave rise to the single market for crowdfunding.

The data is published in the 2025 edition of European Community Capital Landscape 2025 (ECCL 2025), the report produced by Over Ventures in collaboration with Italian Tech Alliance.

The report considers public equity campaigns promoted by start-ups, innovative SMEs and renewable energy projects on ECSP-authorised platforms, excluding real estate crowdfunding, to focus on the borderline area between retail investments, venture capital and private equity.

During 2025, the European market showed signs of solid, structural growth. In addition to the increase in overall volumes, the number of successfully completed campaigns grew by 11.3% compared to the previous year. The average amount per round stood at €789,000, with a median value of €468,000, while 95 transactions, accounting for approximately 27% of the total, exceeded the threshold of €1 million raised. Equity crowdfunding is thus consolidating its position as a complementary and increasingly integrated tool compared to traditional venture capital paths.

A further indicator of market maturity is the increase in the median ticket size of investors, which rose from €3,300 in 2024 to €3,602 in 2025, representing growth of 9.2%. This figure reflects the gradual professionalisation of the investor base and greater involvement of business angels, family offices and institutional investors alongside the retail component.

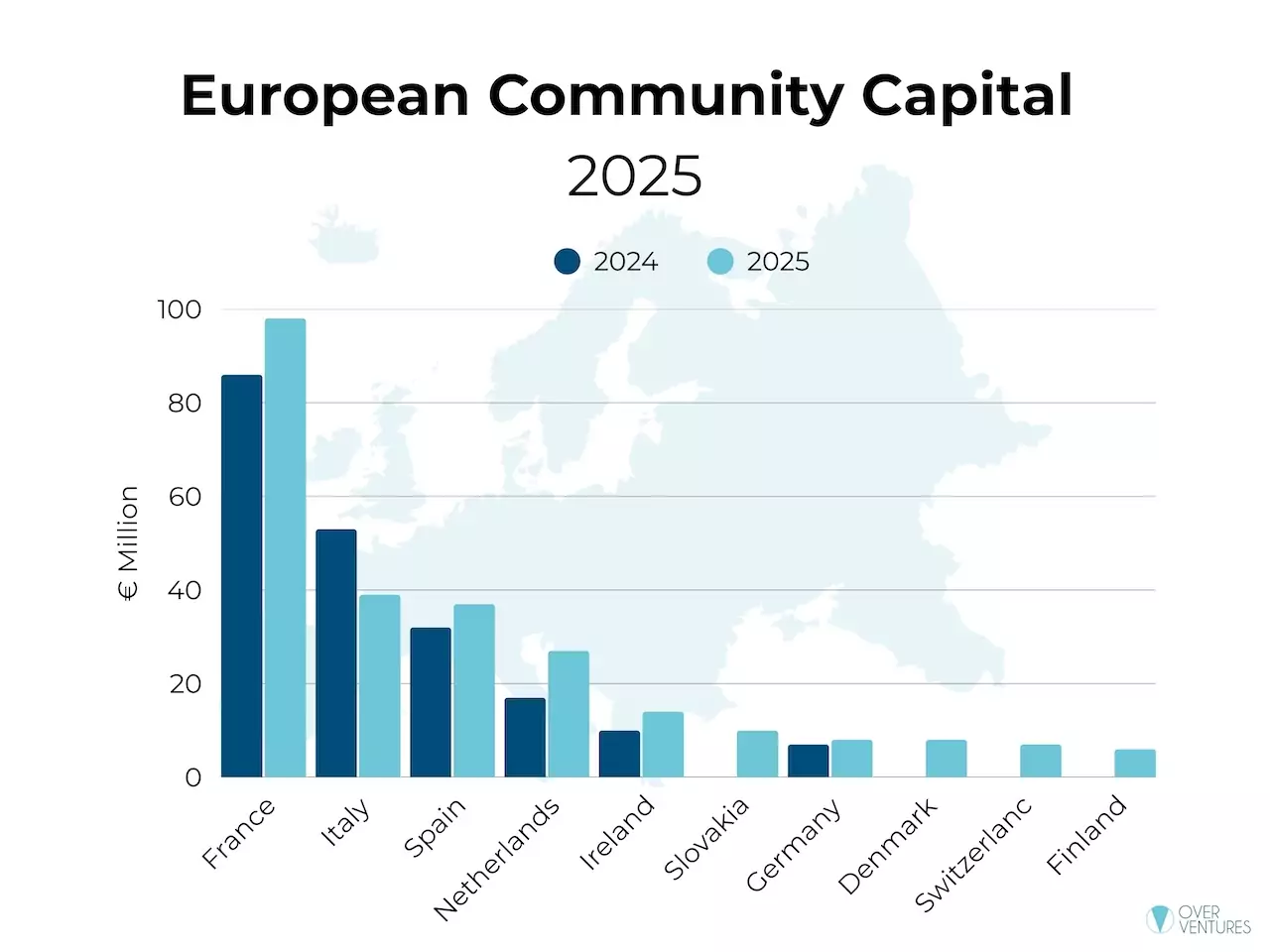

France remains the leading European market in terms of capital raised, with €98.3 million, equal to 35.2% of the total, distributed across 106 campaigns. The French platforms SoWeFund and Tudigo are among the main players of the year, albeit in a context that is still strongly domestic and French-centric.

Italy remains in second place in Europe, with €39.4 million, but it is the only country among the major markets to record a decline in capital raised in 2025. Compared to 2024, capital raised through public equity campaigns fell by approximately 25%, equal to €13.6 million and 13 fewer campaigns on an annual basis.

The slowdown in volumes also reflects a period of regulatory adjustment. The tightening of compliance requirements by Consob and the Bank of Italy has triggered a process of consolidation among domestic portals which, in the short term, has affected market operations but which, in the medium term, is aimed at strengthening market solidity and investor protection.

Compared to other European countries, Italy still suffers from limited integration between equity crowdfunding and venture capital, which is present in France and Spain. However, there are encouraging signs of internationalisation emerging in our country. In 2025, there will be an increase, albeit still modest, in cross-border rounds for Italian start-ups, which are beginning to take advantage of the ECSP passport to access European investors through international platforms.

In Europe, Spain, the Netherlands and Ireland follow France and Italy in terms of market size. Some emerging markets show higher average rounds, while Germany is an anomaly: despite the weight of the German economy, the ECSP market remains limited to €8.1 million over seven campaigns, as most equity crowdfunding activity continues to take place outside the European framework, under the national regime, by way of derogation.

Among the platforms, 2025 marks the overtaking of Capital Cell, which, with €36.7 million raised across 28 campaigns, ranks first in Europe in terms of capital brokered, thanks to its strong specialisation in life sciences and a marked cross-border focus. Crowdcube remains the leading European operator in terms of number of campaigns, while SoWeFund emerges as the most efficient platform in terms of average fundraising per transaction. Invesdor continues its growth trajectory, combining volume development with its first significant exits.

Good results for Italian companies CrowdFundMe and Mamacrowd: the former ranks third among European platforms in terms of number of campaigns carried out (behind Crowdcube and Capital Cell), while the latter ranks fourth. The data confirms the central role of Italian platforms in terms of activity and deal flow, despite lower average rounds compared to other European markets.

From a sectoral perspective, life sciences remain the leading sector in terms of capital raised, followed by food and agriculture and tech, the latter driven by the growing presence of start-ups linked to artificial intelligence. Sectors such as smart cities, software and fintech are showing steadily increasing volumes, confirming crowdfunding’s ability to tap into major technological trends.

In 2025, the role of club dealing platforms and private campaigns reserved for investor communities and business angel clubs, also authorised under ECSP, will be strengthened. This segment, which is not included in the scope of the report, represents a potential multiplier of overall volumes and will be analysed in future editions of the ECCL.

“2025 marks a milestone for European equity crowdfunding,” comments Giancarlo Vergine, founding partner of Over Ventures, in a statement. “More capital, more structured rounds and an increasingly sophisticated investor base confirm that this tool can steadily complement venture capital and angel investing. Even one of Europe’s biggest unicorns, Revolut, started out through crowdfunding, generating significant returns for some of its early investors. High risks remain, but the potential for growth and participation in innovation is now clear.

“We involved key players in the Italian innovation ecosystem to understand the role of community capital at European level,” adds Francesco Cerruti, director of Italian Tech Alliance. “The data contained in the report presented today is essential for navigating a rapidly expanding market with ample room for growth. The sentiment among operators reveals a clear demand: greater integration with venture capital and an integrated, strategic plan at European level.”

ALL RIGHTS RESERVED ©