Partech, a global technology investment firm, has published its annual Africa Tech Venture Capital report, which provides one of the most comprehensive analyses of the continent’s technology funding landscape. The report offers an in-depth look at a rapidly evolving ecosystem that continues to mature, adapt and chart its own course.

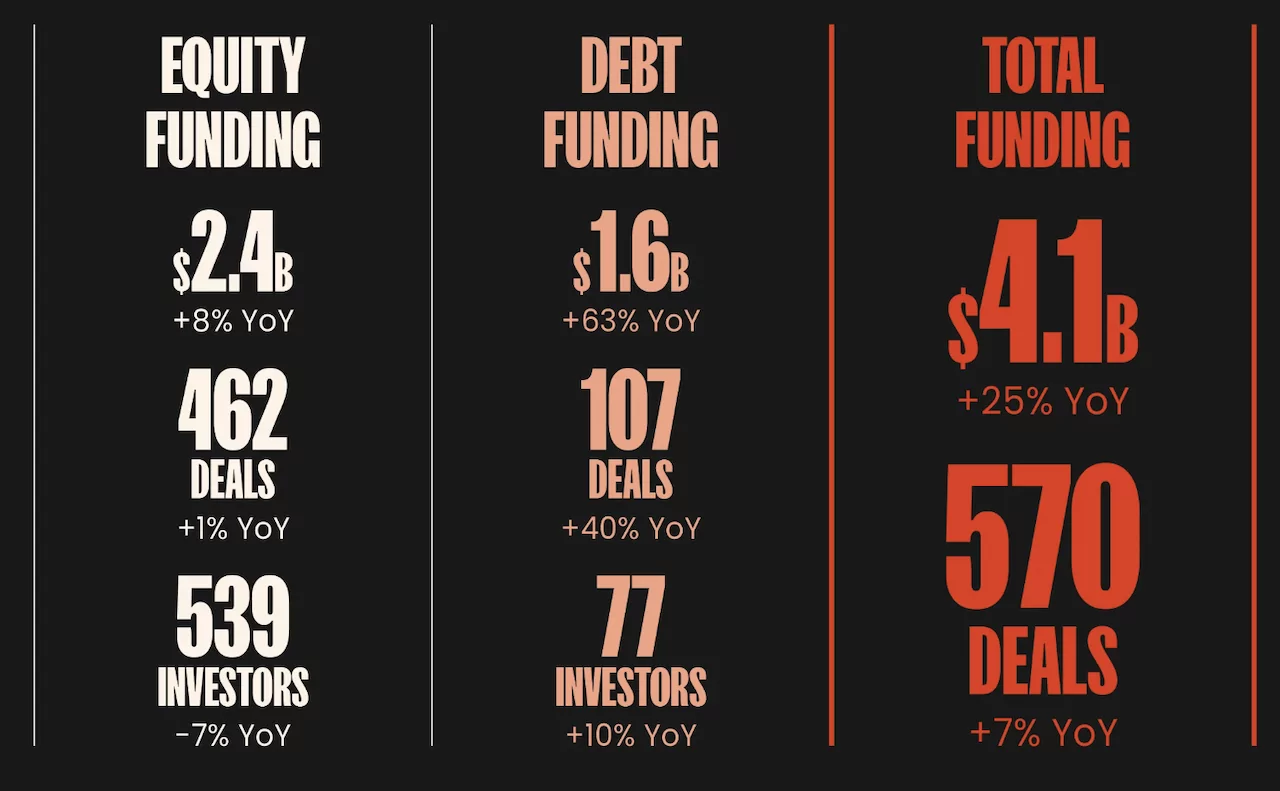

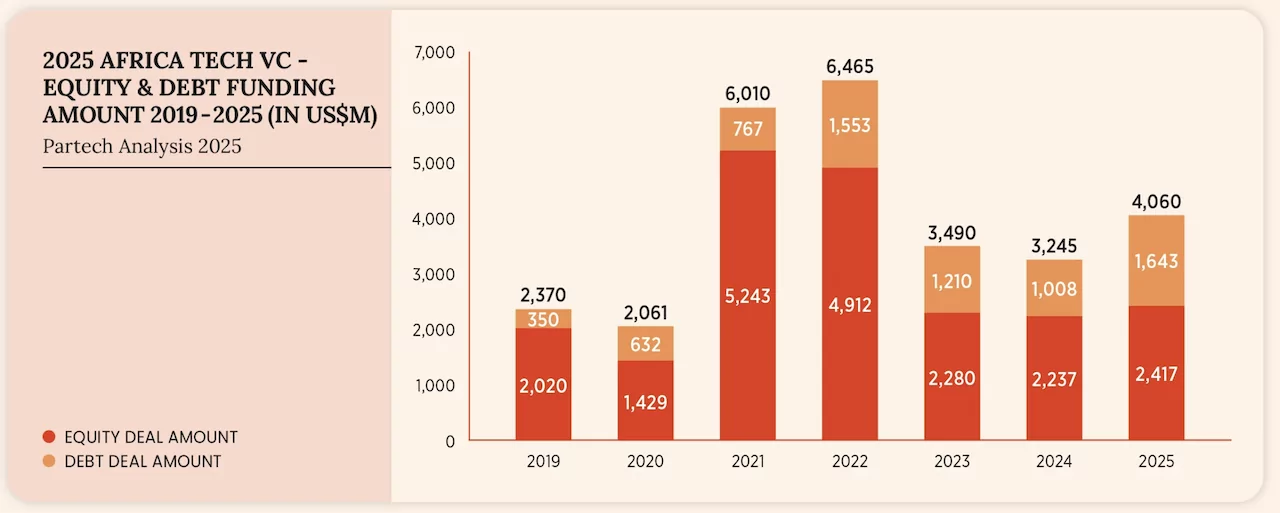

In 2025, African technology funding regained momentum, recording $4.1 billion in combined equity and debt financing (+25% year-on-year). This marks a decisive change after the global and regional slowdown of 2023–2024.

“This year’s recovery highlights the resilience of African entrepreneurs and the growing sophistication of capital markets across the continent,” said Tidjane Dème, general partner at Partech Africa, in a statement. . “Debt capital reached an all-time high, with $1.64 billion raised, and the number of debt transactions rose from 77 to 107 (+39% year-on-year), marking the highest level ever recorded. Meanwhile, equity markets stabilised, with significant recoveries in Series A and B rounds. These indicators reflect a healthier and more mature ecosystem.”

Debt financing was the most notable trend in 2025, with $1.6 billion invested (+63% year-on-year) and 107 debt transactions recorded (+39% year-on-year), the highest level ever recorded. Debt accounted for 41% of all capital invested, up from 31% in 2024 and 17% in 2019.

While equity financing remained largely stable (+8% year-on-year), deal sizes grew at every stage. Series A and B rounds saw the strongest recovery, with average round sizes increasing by 21% and 12% respectively.

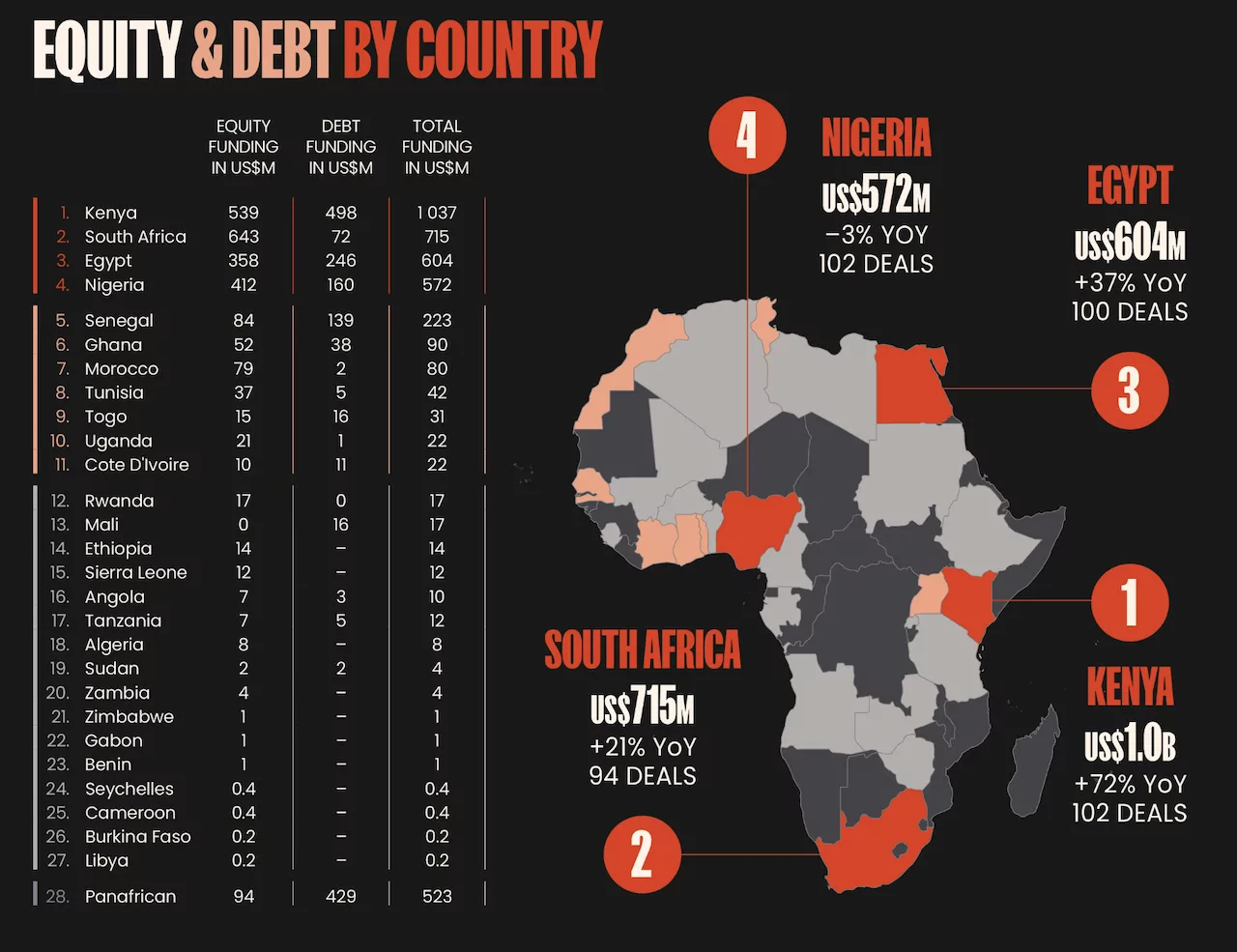

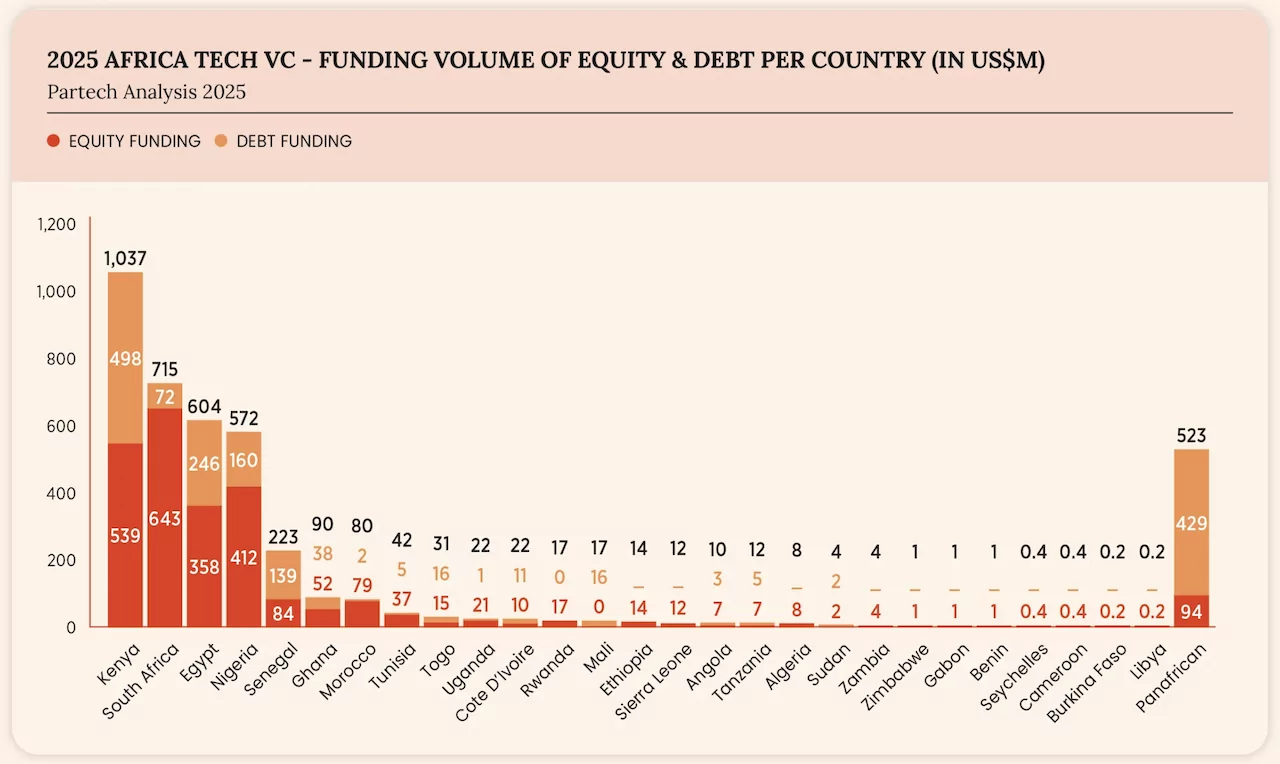

Four ecosystems—Kenya, South Africa, Egypt, and Nigeria—absorbed 72% of total capital, confirming the persistence of a hub-driven VC landscape. While Kenya ranked first with $1.04 billion raised (+72% year-on-year), supported by its ability to attract large debt rounds and multiple megadeals, South Africa regained its leadership in equity deal flow. Nigeria remained very active despite lower absolute volumes, and Egypt maintained a strong pipeline with increasing ticket sizes.

“2025 was the first year since 2017 in which South Africa led the rankings in terms of both equity financing and equity transaction activity in Africa, with a single megadeal accounting for 15% of total financing,” comments Cyril Collon, who edited the report. . “This performance reflects a market where equity growth is driven by a sustained flow of transactions across all stages, rather than a limited number of exceptionally large rounds, and South Africa is the most obvious example of equity-led normalisation.”

In addition to the top four, Senegal, Morocco, and Ghana were the only ecosystems to exceed £50 million in equity funding, highlighting the sharp decline in funding outside the leading markets.

Francophone Africa strengthened its position outside the top four, capturing 68% of equity financing and 64% of transactions, a significant increase compared to 2024.

Fintech continued to dominate with $769 million raised (25% of equity funding), although its overall share declined. Other sectors saw significant growth: cleantech: £400 million (+186% year-on-year), healthtech: £150 million (+232% year-on-year) and enterprise: £170 million (+55% year-on-year). This marks the first time since 2021-2022 that several non-fintech sectors have exceeded £200 million in annual equity financing, signalling greater maturity in the ecosystem.

Startups founded by women increased their share of equity deals to 19% (+8% year-on-year) and captured 10% of total equity funding, although the overall gender gap remains significant.

Investor participation declined again in 2025 (-7% year-on-year), mainly due to the contraction in seed+, while Series A and B saw renewed interest. Investors also diversified beyond fintech, with increased activity in the enterprise, cleantech and agritech sectors.

ALL RIGHTS RESERVED ©