Table of contents

- Investment trends: venture capital quadruples, but Italy slips down the European rankings

- Fewer deals, larger deals. 2025 marks the market’s coming of age

- With AI leading the way, capital is shifting towards deep and strategic technologies

- Central Italy is gaining momentum, whilst the north-west remains the heart of the ecosystem

- Exit: the unresolved issue of public procurement

- Revenue has increased tenfold over the past decade, but is set to slow in 2025

- Investors: institutional investors are on the rise, but domestic capital still dominates

- Universities: Bocconi and the Polytechnic are driving the new wave of entrepreneurship

‘State of Italian VC’, the analysis of the evolution of the Italian innovation industry produced by P101, is now in its tenth edition and reveals that Italian venture capital has been growing for over a decade, following a trajectory that has led to the development of an industry which, over this period, has invested around €10 billion in innovation in the country.

This industry now comprises more than 14,000 innovative companies (including those founded after 2010, the year considered a benchmark for the start of the structural development of the VC sector in Italy), of which almost 12,000 are start-ups, which in 2025 generated a production value of €10 billion and employed around 62,000 people. Of these, around a third work in start-ups which, last year alone, recorded a production value of approximately €2.8 billion.

“Today we are witnessing the evolution of an industry that, a decade ago in Italy, effectively did not exist. We have gone from a handful of operators with limited resources and marginal impact to a venture capital firm with solid foundations that consistently invests between one and two billion a year in the real economy,” says Andrea Di Camillo, founder and managing partner of P101, in a statement. “The context has also changed radically: the era of incremental innovation is over. Today we are facing a major technological shift, with AI and critical infrastructure redirecting the flow of capital, whilst there is a growing realisation that digital sovereignty is no longer a choice, but an absolute necessity. Everything is moving faster, and if we want to keep pace, the capital we are seeing grow – thanks to the support of institutional investors such as CDP and the EIF and players such as Azimut – will not be enough. We will need corporations, whose activity remains limited to exemplary cases, and a more efficient public capital market. But above all, an international perspective will be needed: from funds, which must look beyond national borders; from companies, which must compete globally; and from investors, who must become increasingly international. In a continent that remains too fragmented, the future of this industry – central to innovation – depends on a greater recognition of VC as a European asset class, and the 28th regime is a first step forward in this direction.”

Investment trends: venture capital quadruples, but Italy slips down the European rankings

Over the past ten years, Italian venture capital firms have invested a total of around €10 billion in start-ups, €7.5 billion of which has been invested in the last five years. The industry’s growth trajectory has led to a fourfold increase in the country’s capacity for investment in innovation, rising from €363 million in 2016 to €1.4 billion in 2025.

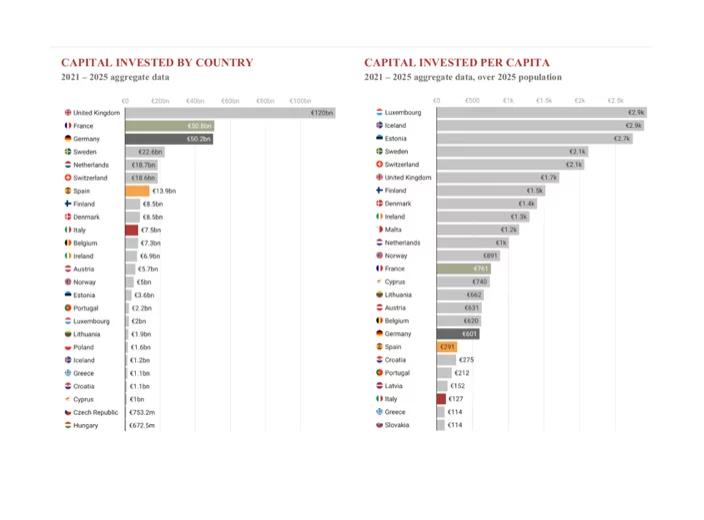

Despite this growth, there remains considerable scope for further development. Indeed, although Italy is Europe’s fourth-largest economy, per capita investment in venture capital remains disproportionately low: in 2025, it stood at just €127, causing Italy to be overtaken by Lithuania and slip to third-last place in Europe in this ranking, ahead of only Greece and Slovenia.

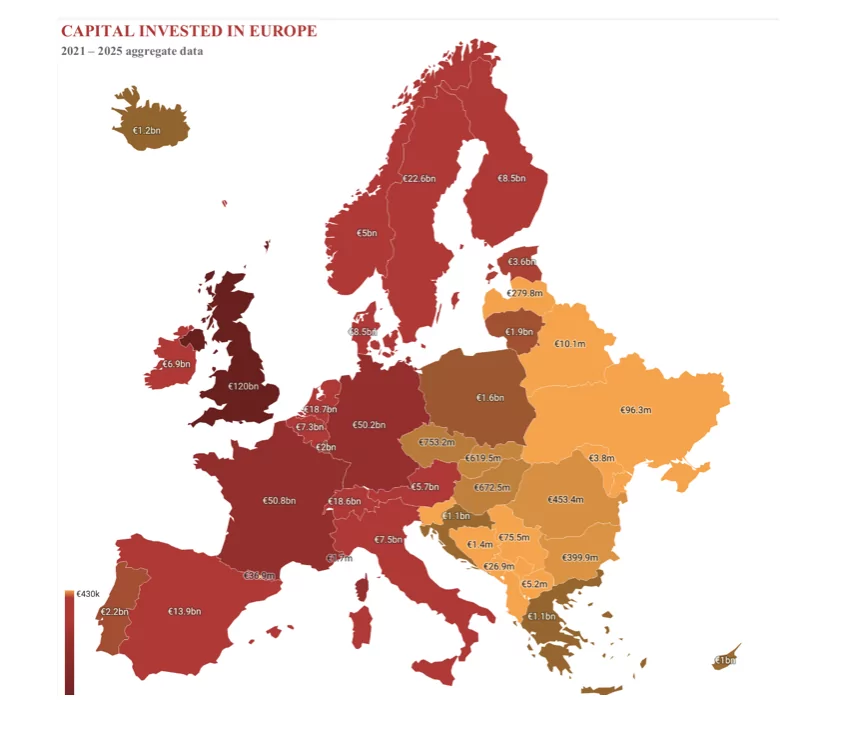

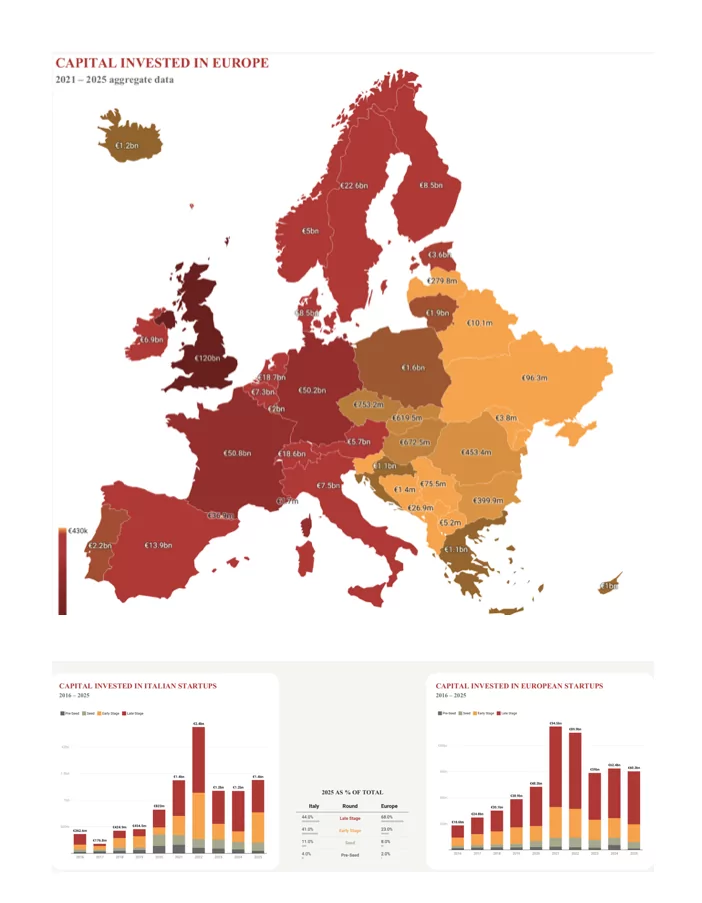

Looking at the European picture, over the last five years, venture capital has invested around €367 billion (€527 billion over ten years). A third of these investments were made in the UK (€120 billion), followed by France (€51 billion) and Germany (€50 billion), figures that highlight the level of maturity achieved by the most advanced ecosystems.

Fewer deals, larger deals. 2025 marks the market’s coming of age

In 2025, investment in Italy reached €1.4 billion, up 17% on 2024 despite a lower number of transactions, which fell to 637 (-35%); this trend highlights an increase in the median transaction size, which in Italy doubled to €1 million compared with 2024.

More specifically, early-stage investment has risen sharply to €568 million (+186%), whilst late-stage investment has fallen by 20% to €606 million. Seed funding has increased to €155 million (+9%), whilst pre-seed funding has continued its downward trend, falling to €48 million (-32%).

With the volume of investment on the rise, Italy is bucking the European trend: whilst Europe saw around 13,000 deals (-32%), investment totalled 60 billion, a slight decline (-3%).

Europe bucked the trend even against the backdrop of a rapidly growing US market (+44%), which reached €285 billion on the back of around 21,000 deals (-13%).

The average valuations of Italian start-ups have risen over time, from €1.8 million in 2016 to nearly €5 million in 2025. This figure is half that seen across Europe, which in turn remains significantly lower than in the US, where the average valuation stands at nearly €49 million.

With AI leading the way, capital is shifting towards deep and strategic technologies

In 2025, the venture capital sector is also seeing a boom in artificial intelligence and machine learning, which have attracted investments of nearly half a billion euros – double the figure for 2024 – and recorded impressive growth over the five-year period (+421% compared to 2021).

Despite this growth, Italy still lags behind the rest of Europe in this respect, with France leading the way by investing €3.7 billion in the sector, followed by Germany with €3.3 billion.

The gap becomes staggering when looking at the US, where in 2025 venture capital firms doubled their investment in AI and ML, bringing the total to over €155 billion – more than seven times the amount invested in Europe (€21 billion) and 300 times the amount invested in Italy.

Turning to Italy, healthcare-related sectors have seen structural growth, with the life sciences sector reaching €341 million (+99%) and healthtech €283 million (+127%), followed by big data, a sector which recorded the most significant growth in 2025 (+711%), attracting €260 million, followed by cybersecurity at €197 million (+275%).

In 2025, Italy saw a continuation of the trend towards a shift in capital from sectors linked to the digital world in general towards strategic, high-tech sectors

Central Italy is gaining momentum, whilst the north-west remains the heart of the ecosystem

The increase in investment in 2025, which rose to €1.4 billion, is attributable to central Italy, where the amount invested tripled to €435 million.

Investment in the north-east has fallen to €97 million, as has investment in the north-west, which nevertheless remains the hub of the national ecosystem with investment totalling €834 million.

In the south and on the islands, activity remains limited, with the south at €69 million and the islands at €5 million.

Exit: the unresolved issue of public procurement

In 2025, Italy recorded 22 exits, down from 31 in 2024 due to a decline in corporate acquisitions (from 25 to 14 deals).

The number of buyouts rose from 6 to 8, indicating a growing role for financial investors, whilst, as in 2024, there were no IPOs by companies backed by venture capital.

Over the past decade, only 22 IPOs in Italy have involved venture capital-backed companies, confirming the limited role of public markets in the industry. Such exits are rare even in Europe, where only 12 were recorded in 2025 out of a total of 227 IPOs; this figure rises to 52 in the US.

Across Europe, the number of exits remained broadly stable at around 1,000, whilst in the US they rose to around 1,500 (+13%).

Revenue has increased tenfold over the past decade, but is set to slow in 2025

In 2025, capital raised across nine funds reached nearly €400 million (down 13% year-on-year), with the market focusing on smaller funds, none of which exceeded €150 million.

In Europe, total raise reached almost €11 billion, a sharp decline from the €25 billion recorded in 2024.

In total, over €8 billion was raised in Italy over the decade through 123 funds (here, the figure refers to funds that began raising capital from 2016 onwards, whilst the total amount invested over the decade – €10 billion – includes funds that had begun raising capital earlier).

Although Italy has doubled its fundraising capacity over the past ten years, it still accounts for only a small fraction of the total raised in Europe, which has been driven over the decade by countries such as Germany and France (both at €32 billion), each of which has raised almost four times as much capital as Italy over the same period. Spain, too, with €12 billion, outstrips Italy, which ranks 8th in the continent’s fundraising league table.

The growth in fund sizes, increasingly driven by institutional investors, will be crucial to strengthening Italy’s capacity to invest in innovation and keeping pace with the European countries that currently dominate the sector.

Investors: institutional investors are on the rise, but domestic capital still dominates

Italian venture capital continues to rely heavily on domestic investors (71%). These are followed by European investors (19%) and North American investors (4%), whilst there are no Asian investors. A relatively high proportion of investors from the Middle East (6%) is evident, making Italy the only major country on the continent to receive a significant contribution from that region.

Whilst the data highlight Italy’s limited international diversification, the composition of Italian LP funds reflects a relatively balanced structure. Direct investment accounts for 17%, bank investment for 15% and fund-of-funds investment for 14%. Italy also sees a relatively high level of investment from foundations (10%) and pension funds (9%). The contribution from insurance companies (4%) and corporations (12%) remains limited; in countries such as France, these account for 14% and 21% respectively.

Spain stands out for the prominent role played by economic development agencies (13%), a sector that is virtually non-existent in Italy (1%).

In general, interest from institutional investors is growing steadily, thanks to the support of investors such as CDP, FEI and Fondo Italiano – which have invested in Italian funds 63 times over the past 10 years – and Azimut, as well as being driven by new regulatory measures designed to encourage investment in venture capital.

The challenge now extends beyond Italy’s borders: the country will need to make itself more attractive to international investors.

Universities: Bocconi and the Polytechnic are driving the new wave of entrepreneurship

Over the past five years, start-ups founded by former students of Italy’s leading universities have raised over €7.3 billion, with funding provided by the wider innovation ecosystem, which, alongside Italian venture capital firms, includes business angels, private investors, foreign investors and corporate investors.

Bocconi University (€3.1 billion) and the Politecnico di Milano (€2.2 billion) top the rankings (and have also jointly established the Tech Europe Foundation to further strengthen their position), followed by the University of Bologna (€1 billion). LUISS (€505 million), La Sapienza University of Rome (€338 million) and the Polytechnic University of Turin (€196 million) contributed with more modest but significant investment flows.

ALL RIGHTS RESERVED ©