Pitchbook has released preliminary figures on investment trends, exits and venture capital fundraising during the first quarter of 2026 in Europe, the US and the Asian market.

Europe

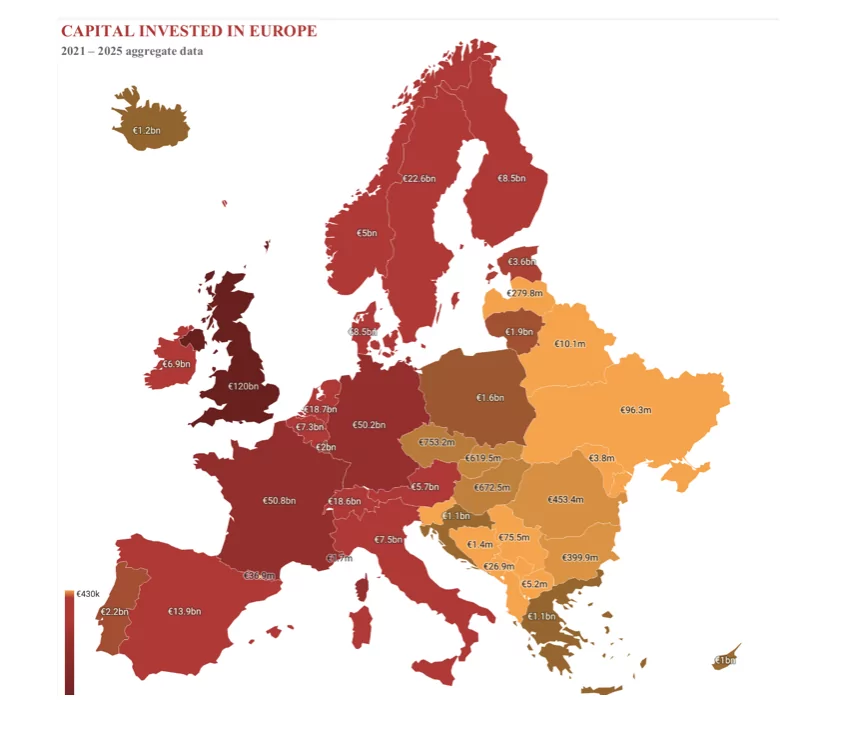

Investment activity in Europe got off to a record-breaking start this year, driven by several large-scale funding rounds involving start-ups in the artificial intelligence sector. The five largest deals accounted for around 25% of the total value of European investments: these were Nscale, Naura Robotics, Wayve, Cloover and Advanced Machine Intelligence.

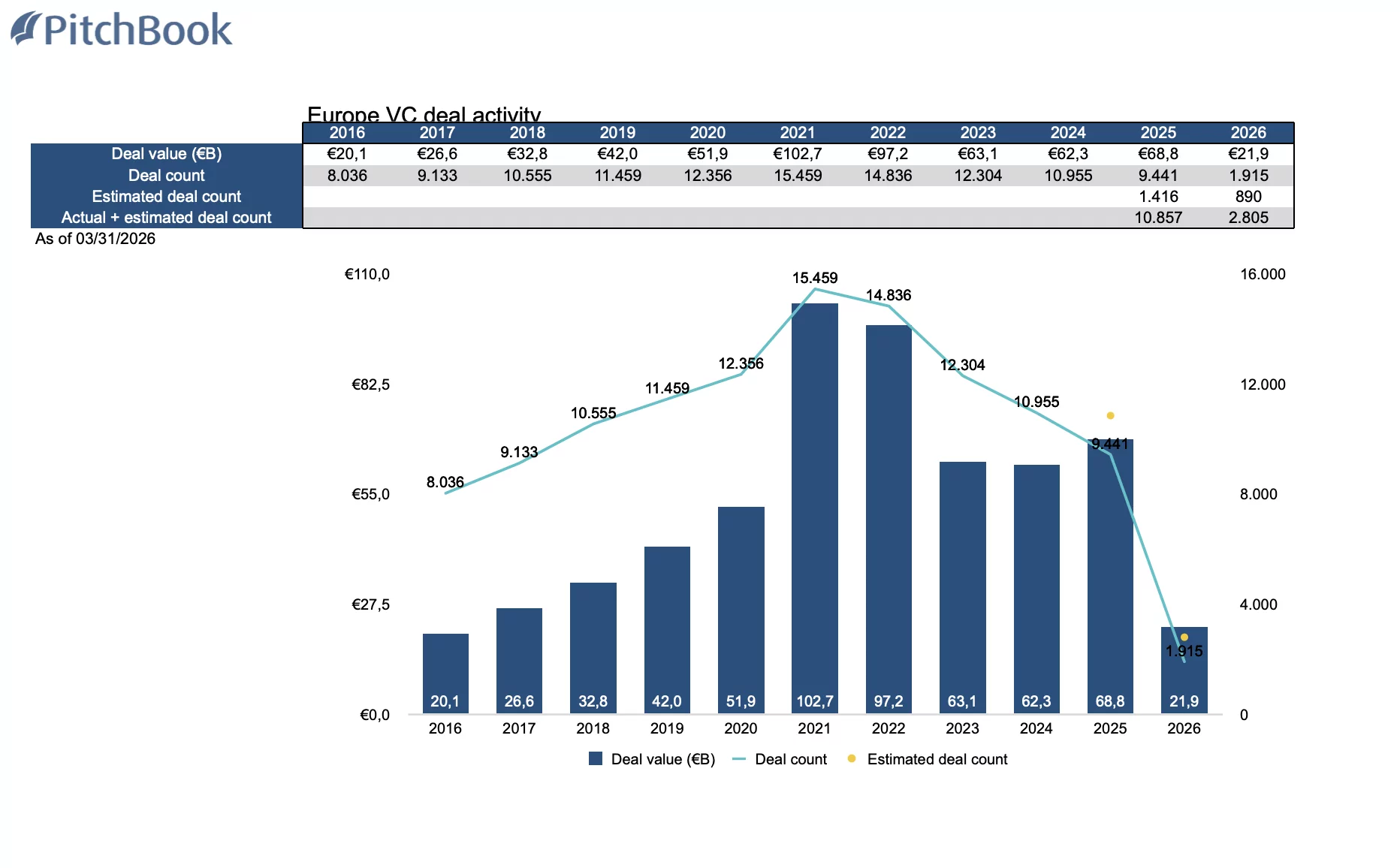

The proportion of capital invested in AI-related activities relative to the overall ecosystem has also grown, indicating an increasing reliance on AI-driven deals. 61.3% of the value of deals in Europe, amounting to €13.4 billion, and 38.9% of the number of deals (744) were completed in AI start-ups. The total amount invested in Europe in the first quarter of 2026 is therefore €21.9 billion spread across 1,915 deals (the fourth quarter of 2025 recorded €20 billion in investment across 2,126 deals).

Exit activity in the European venture capital sector got off to a steady start in the first quarter of 2026, with both value and volume reaching levels comparable to those of recent quarters, although volatility persists. At €16 billion, the quarter did not see the kind of major exits observed in the United States, but it did see the completion of several billion-euro exits.

The VC fundraising landscape in the first quarter of 2026 remained subdued, with figures broadly in line with the weak performance of 2025 against a backdrop of challenging fundraising conditions. Only €3.5 billion was raised across 37 funds, with both figures close to their lowest levels in the last ten years.

USA

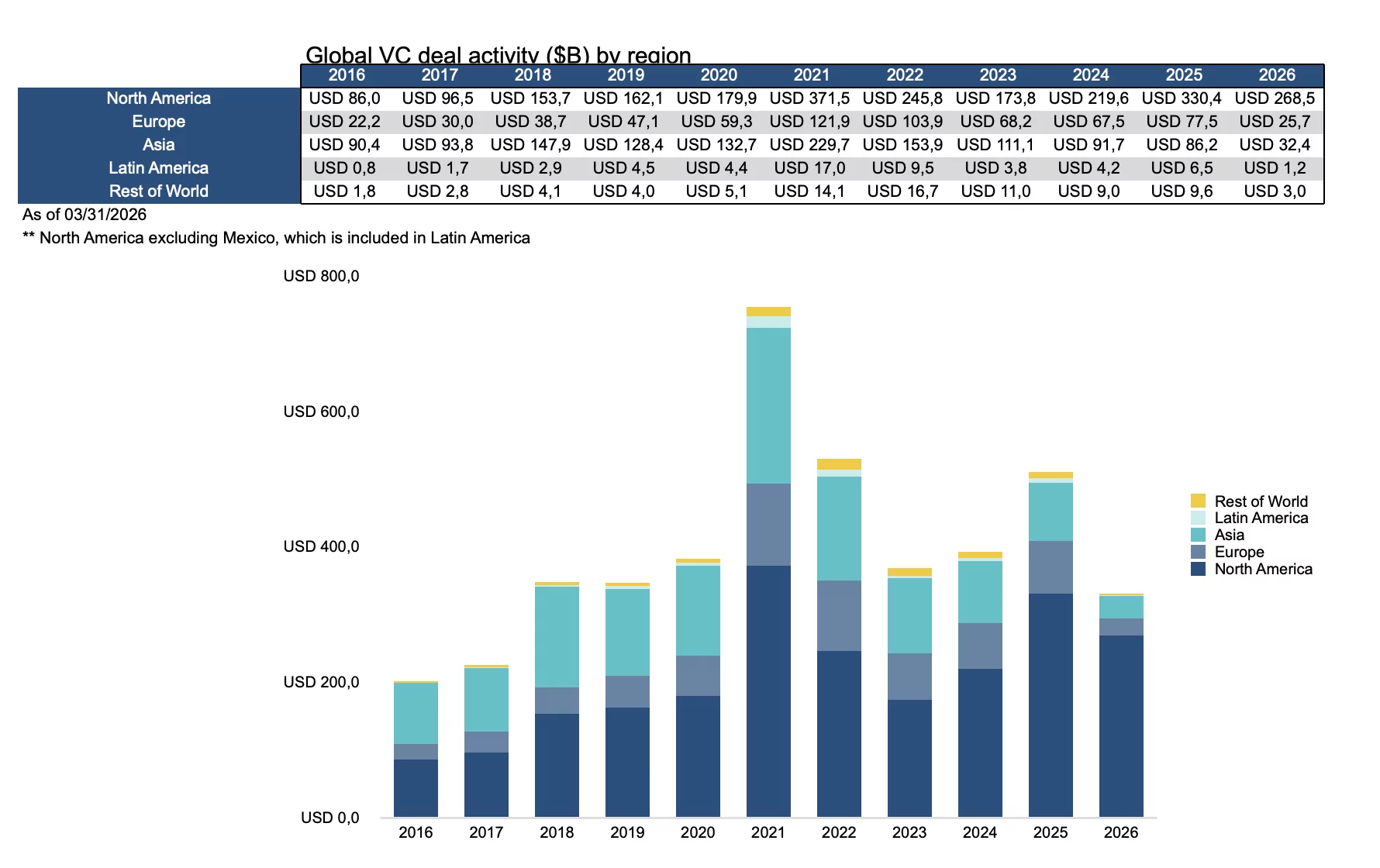

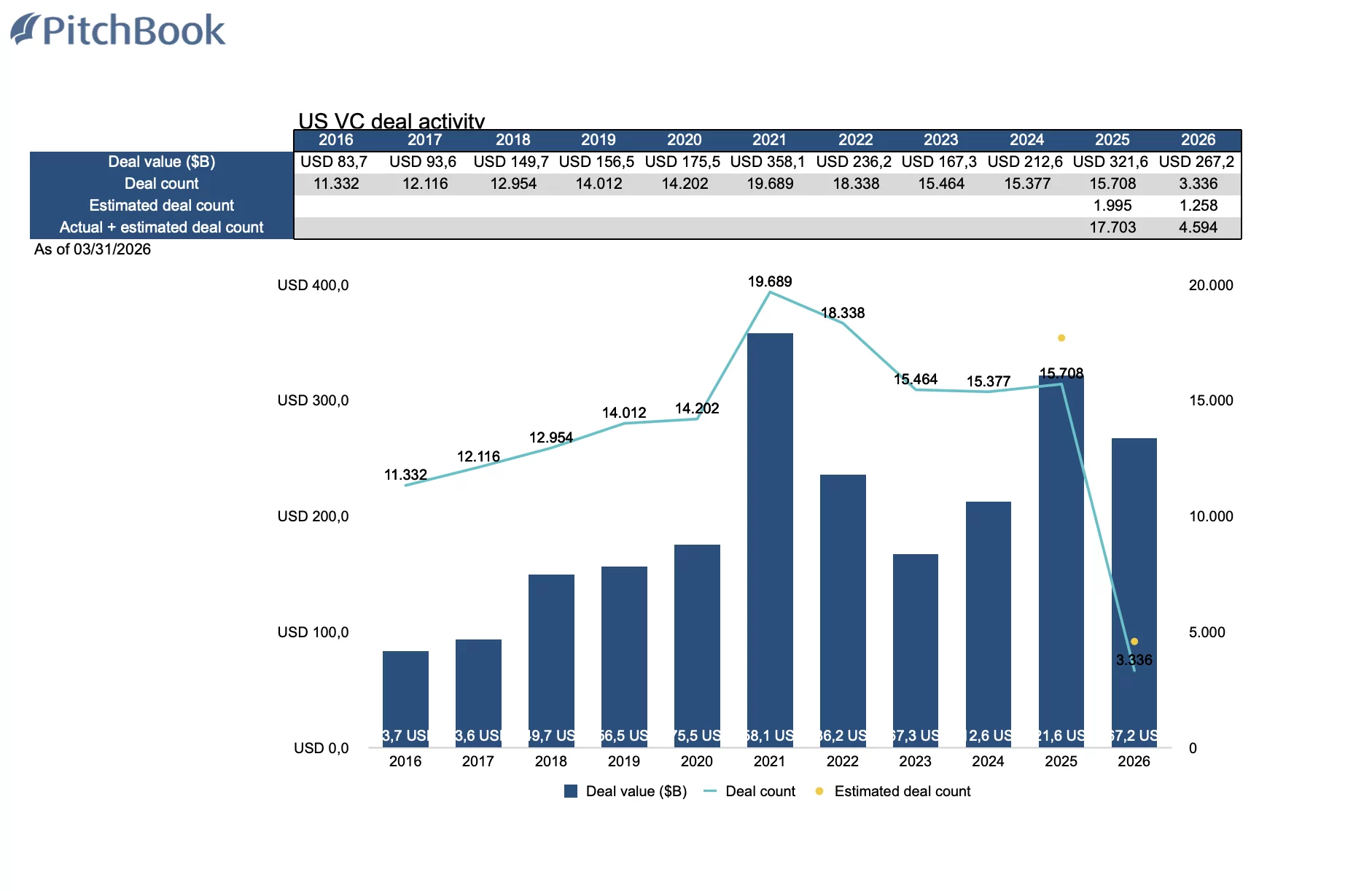

During the quarter, deals worth $267.2 billion were closed in the United States, more than double the figure from the previous record quarter. However, this figure is highly concentrated, with $122 billion raised by OpenAI, $30 billion by Anthropic, $20 billion by xAI and $16 billion by Waymo. Databricks’ $7 billion funding round rounded out the top five deals, and together these deals accounted for approximately 73% of the total deal value for the quarter. Excluding these deals, the $72.2 billion in investment still represented a strong quarter, as evidenced by the estimated 4,595 deals closed during the quarter. The figure of $72.2 billion is in line with recent quarters.

AI continues to be the focus of venture capital, and this sustained growth is, more than anything else, a sign that AI is no longer an optional extra for companies, but a necessity for attracting the interest of tech investors. 88.8% of the value of deals went to AI companies during the quarter. These companies span the full range of sectors and verticals, from healthcare and life sciences to enterprise technology and consumer products.

The first quarter of 2026 generated an exit value of $347.3 billion, the highest quarterly total on record and already the second-highest annual figure in history, surpassed only by 2021. But a single transaction accounts for much of this story: SpaceX’s $250 billion acquisition of xAI, a merger of two of Elon Musk’s companies, accounts for 72% of the quarter’s total. Excluding this, the exit figure stands at a more modest $97.3 billion, which is still the highest quarterly figure since the fourth quarter of 2021.

AI-focused M&A activity accounted for the bulk of the value of exits in the quarter. Apart from SpaceX, Google’s $32 billion acquisition of Wiz is the largest corporate acquisition of a VC-backed company ever recorded. Marvell Technology acquired the AI connectivity start-up Celestial AI for $6 billion, and Palo Alto Networks acquired the Chronosphere platform for $3.4 billion.

The IPO market continues its slow and selective recovery. The 15 VC-backed listings in the first quarter put 2026 on track for a total of 60, exceeding the 50 recorded in 2025 but well below what is needed to clear the backlog that has built up over the years. The potential IPOs of SpaceX, OpenAI and Anthropic, each of which would rank among the largest in history, could generate an exit value greater than that of all VC-backed IPOs combined since 2000. A positive reception would likely catalyse a broader wave of listings and inject much-needed liquidity into a market that has remained largely frozen since 2022. But the risk is twofold: if these mega-IPOs were to saturate underwriting capacity and institutional capital, the broader window for IPOs could be pushed back to 2027, prolonging the liquidity drought for the rest of the market.

VC fundraising is recovering on paper, but the overall figure overstates the extent of that recovery. Although the $47.8 billion represents a significant increase compared with recent quarters, the amount remains heavily concentrated in mega-funds. Thrive Capital’s $9 billion growth fund, the largest of the quarter, accounted for nearly 19% of all commitments closed. This underscores that capital formation remains heavily concentrated amongst a small number of large managers.

LP capital continues to flow disproportionately towards established managers with proven track records, widening the gap between the top tier of the market and the rest. Institutional LPs are facing a challenging environment: evolving regulatory frameworks, heightened geopolitical tensions and a prevailing allocation to this asset class; as a result, they are increasingly turning to the best-known vehicles.

APAC

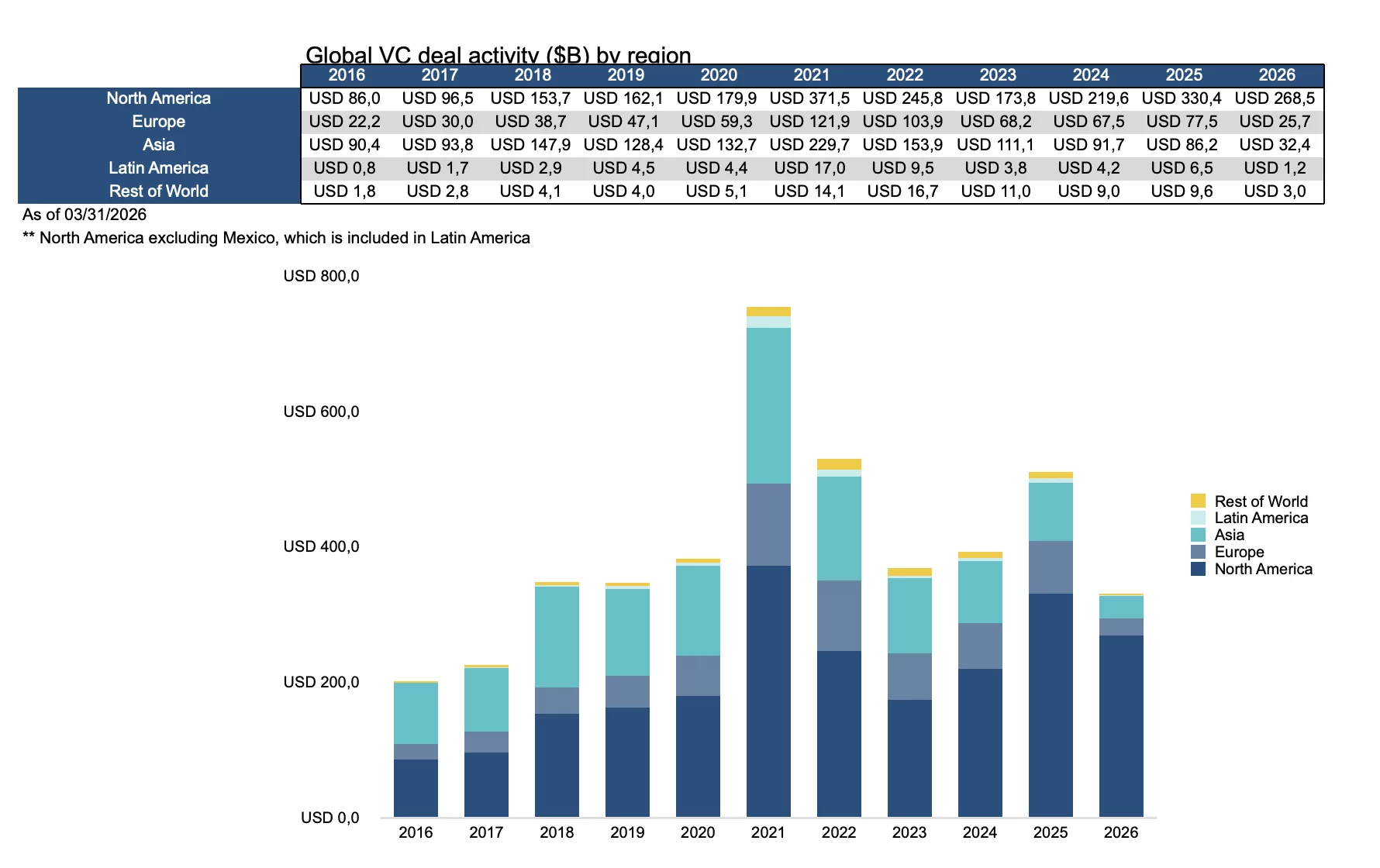

Venture capital investment activity in Asia in the first quarter of 2026 appears to be in line with recent quarterly trends, with around 3,000–3,500 deals in the quarter since 2023, suggesting a stabilisation following the post- , although the region has not yet recovered the volume peaks of the 2020–2021 cycle and shows no short-term signs of doing so. The first quarter of 2026 saw 2,622 transactions, with a total of $32.4 billion invested.

AI and machine learning account for a structurally increasing share of deal volume in Asia compared with any period prior to 2023. What began as a cyclical shift towards AI increasingly appears to be a permanent reallocation of deal flow away from the consumer internet and fintech sectors that dominated the previous cycle.

Exit activity remains the most obvious constraint on the Asian VC ecosystem. Both the number and value of deals have remained stable or declined since 2023, with no visible reversal of this trend in the first quarter of 2026, squeezing distributions to LPs and placing an increasingly heavy brake on commitments to new funds, a situation particularly acute for managers whose funds are concentrated in the 2018–2021 period. With just $18.7 billion in exit value generated during the quarter, the year is on track to record figures similar to those of the last two years.

VC fundraising closed 2025 with 463 funds and approximately $42 billion raised, whilst preliminary figures for the first quarter of 2026 show just 87 funds with $6.2 billion, reflecting a market in which LPs’ interest in Asia-focused vehicles remains structurally limited rather than cyclically depressed. The persistent gap between ongoing capital deployment and the formation of new funds suggests that the sector is increasingly operating on the basis of pre-existing financial resources.

ALL RIGHTS RESERVED ©