Innovative companies in the life sciences sector raised a total of €414.1 million in 2025, with almost 70% of this amount raised in the second half of the year; 1,591 innovative companies were recorded between 2020 and 2025, accounting for 11.8% of the entire Italian innovation ecosystem, of which 1,229 were start-ups and 362 were innovative SMEs. However, this strong growth in capital is not matched by a proportional increase in the number of new start-ups: in the second half of 2025, there were 131 new life sciences start-ups, essentially stable compared to the second half of 2024, highlighting a phase of greater maturity and selection within the ecosystem. By contrast, the role of AI has grown significantly, accounting for 39.7% of new life sciences start-ups in the half-year, confirming its status as one of the sector’s key technological enablers. This is the picture that emerges from the fifth edition of Listup, the half-yearly observatory promoted by Indicon, in collaboration with Italian Tech Alliance, InnovUp and Growth Capital, dedicated to the Italian ecosystem of startups and innovative SMEs active in the life sciences sector.

“Now in its fifth edition, Listup paints a picture of a life sciences sector that continues to account for around 12% of Italy’s innovation ecosystem,” comments Elena Paola Lanati, CEO of Indicon, in a statement. “The good news is that funding in the sector is growing strongly compared to 2024, reaching almost €420 million in 2025. In this edition, we wanted to complement the Italian analysis with a comparison with France: the French market has around 70% more innovative life sciences companies than Italy, but raises over five times as much capital, with an average raise per company around three times higher than in Italy. This figure highlights the untapped potential of our ecosystem and could serve as a significant stimulus for guiding future decisions in support of innovation in the sector. We have also chosen to present Listup’s findings alongside the ‘Protagonists of Innovation’ award, now in its second year and produced by Innlifes, precisely to highlight Italian excellence in life sciences research, business and investment, and to demonstrate the sector’s potential to contribute to the country’s competitiveness.”

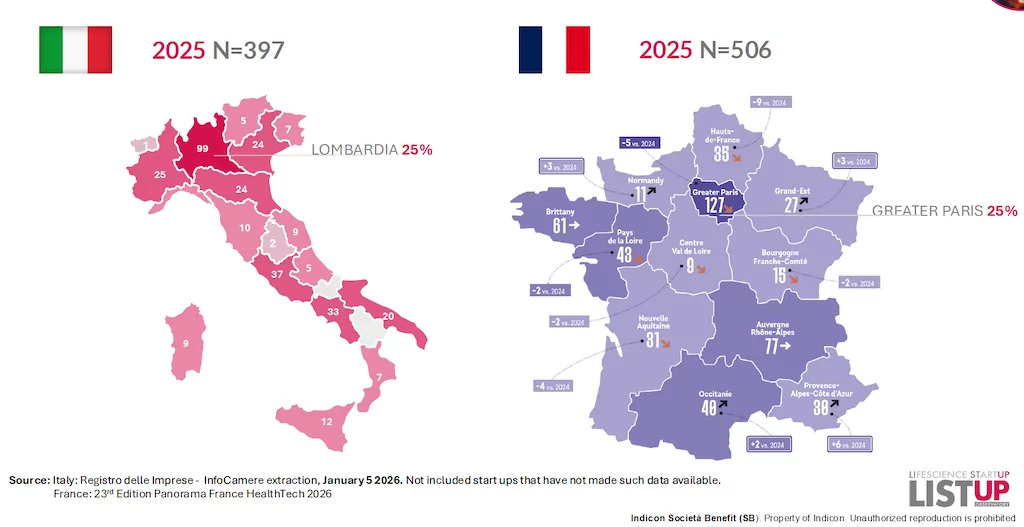

Listup data confirm the strategic role of the life sciences within the Italian innovation ecosystem, even amidst a period of regulatory transition linked to the entry into force of the Competition Bill. Between 2020 and 2025, there were 1,591 innovative life sciences companies, accounting for 11.8% of the national total. In the second half of 2025, the sector accounts for 11.2% of the total, with 166 new companies recorded. The impact of the new legislation is more limited for life sciences than for innovative companies as a whole: the sector recorded a contraction of 9.5% compared to 11.7% of the total. In particular, innovative life sciences SMEs show greater stability, with a 4% reduction, whilst life sciences start-ups recorded an 11% decline. Lombardy remains the leading national ecosystem for innovative life sciences enterprises, accounting for 28.3% of active companies, with Milan remaining the leading hub, accounting for 21.7%, followed by Lazio and Campania.

In the second half of 2025, there were 131 new life sciences start-ups, a figure that remained largely stable compared with the 132 recorded in the second half of 2024 and held up better than the total number of innovative start-ups, which fell by 2.1%. This figure takes on particular significance when viewed alongside investment trends: whilst the number of new start-ups is not growing, the capital raised in the sector is increasing significantly, signalling a progressive concentration of resources on more established companies with advanced pipelines, greater technological strength and higher scalability potential.

Among life sciences start-ups, digital health remains the dominant category, accounting for 48.9% of new ventures in the second half of 2025. Artificial intelligence accounts for 39.7% of new life sciences start-ups in the period, confirming its status as the main technological enabler, whilst telemedicine has grown by 63.6% compared to the second half of 2024, with 18 new start-ups. There were 362 innovative life sciences SMEs in the 2020–2025 period, accounting for 14.6% of all innovative Italian SMEs. In the second half of 2025, the sector recorded 35 new life sciences SMEs, with 31.4% concentrated in Lombardy and Milan accounting for 28.6% of the total. Among SMEs too, digital health and medtech represent the main areas, accounting for 37.1% and 25.7% of new businesses in the half-year.

In terms of ESG and governance, the life sciences sector continues to stand out for having a higher proportion of women than the average: in the second half of 2025, innovative life sciences companies with predominantly female boards accounted for 17.1%, compared with 11.3% of the total. Youth-led governance in the sector is also growing, standing at 14.9% in H2 2025 compared to 10.7% of the total.

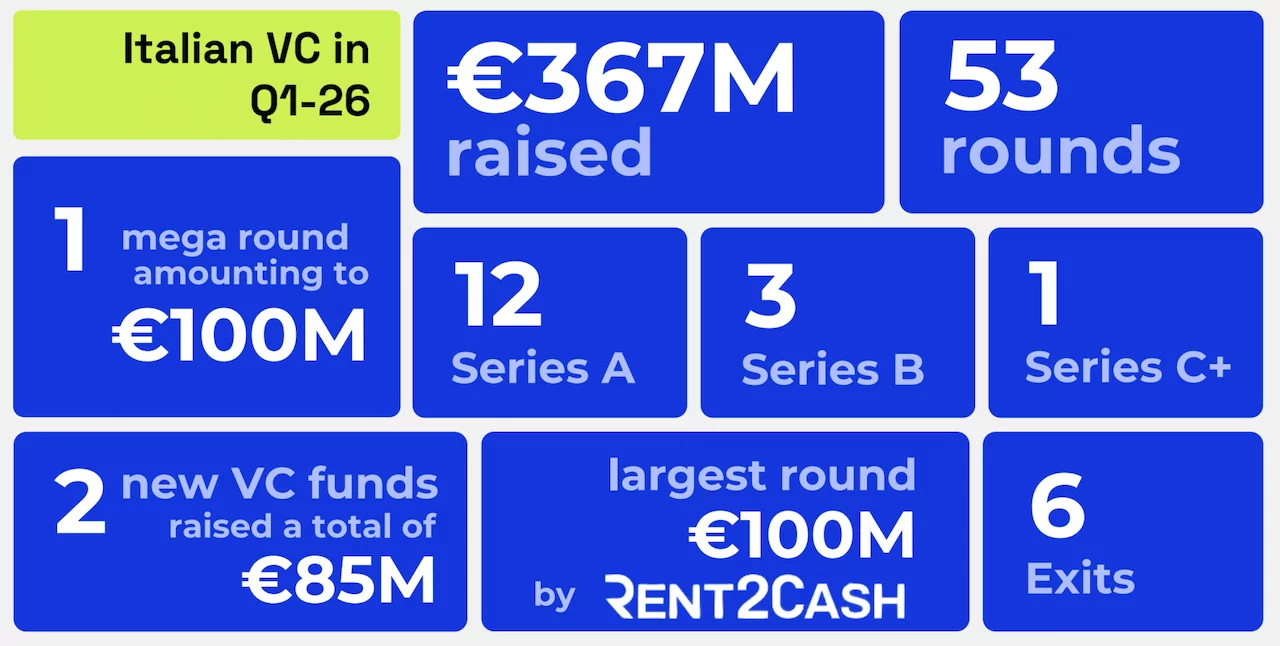

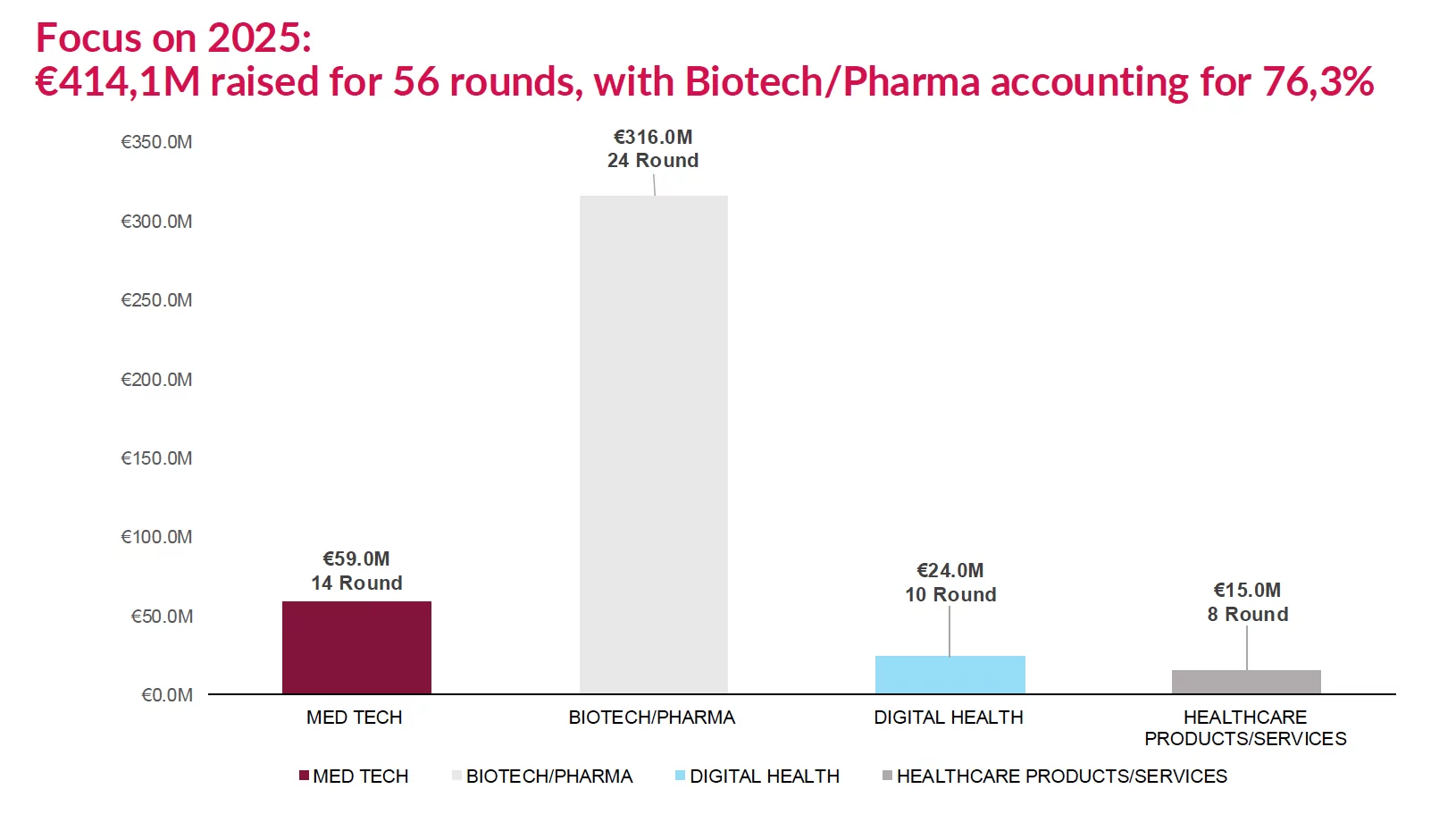

In terms of funding, the life sciences sector remains one of the most attractive sectors for Italian venture capital. In 2025, innovative life sciences start-ups and SMEs raised €414.1 million across 56 funding rounds, the highest figure for the period under review. In the second half of 2025, funding reached €279.5 million across 28 rounds, representing a 135% increase compared to the €118.7 million raised in the second half of 2024 and accounting for approximately 67.5% of the annual total. The average value of funding rounds is also rising: in 2025, the average round size rose to €7.4 million, compared to €4.9 million in 2024; in the second half of 2025 alone, the average value stood at around €10 million per round, more than double the approximately €4 million recorded in the second half of 2024. This trend highlights a significant shift for the ecosystem: the number of new life sciences start-ups remains largely stable, but the capital invested is rising sharply, indicating greater selectivity on the part of investors and a concentration of resources on companies perceived as more mature and scalable.

Fundraising is driven primarily by the biotech/pharma sector, which in the second half of 2025 accounted for 91% of the capital raised, amounting to €254 million. In 2025, the biotech/pharma sector raised a total of €316 million, accounting for 76.3% of the total. The top five rounds by value accounted for 85% of the capital raised in the second half of 2025, confirming the concentration of investment on companies with a strong technological component, advanced pipelines and intellectual property. The report thus highlights a structural gap between entrepreneurial growth, driven primarily by digital health, and the allocation of capital, which remains heavily oriented towards biotech and pharma: in the second half of 2025, digital health accounts for 46.4% of new life sciences companies, yet attracts only 6% of total investment for the half-year.

The digital health sector is cementing its central role: between 2020 and 2025, it accounts for 40.6% of innovative life sciences companies, rising to 46.4% in the second half of 2025. This is followed by healthcare products/services, at 23.5% in H2 2025, medtech, at 19.9%, and biotech/pharma, at 10.2%. Artificial intelligence remains one of the sector’s key technological drivers. Innovative life sciences companies, start-ups and SMEs based on AI account for 38% of new businesses in the second half of 2025, compared with 28.5% in the 2020–2025 period. Telemedicine is also growing, rising from 13% in the 2020–2025 period to 14.5% in the second half of 2025, with 24 new companies in the six-month period. The sector also confirms a strong research component: in the 2020–2025 period, life sciences companies show a higher proportion of registered patents and software compared to the total number of innovative companies, at 31.3% versus 27.4%.

For the first time, Listup also includes a comparison with the French healthtech ecosystem, allowing Italy’s position to be assessed from a European perspective. In France, 2,738 innovative healthtech companies were recorded, compared with 1,591 in Italy over the 2020–2025 period. The gap is even more evident in terms of capital: equity raised in France amounts to €2.3 billion, compared to €414 million recorded in Italy in 2025. The comparison highlights the existence of significant growth potential for the Italian ecosystem, which possesses high-level scientific and technological expertise but needs to further strengthen its ability to attract capital, support the scaling up of companies and accompany start-ups through the scale-up phase. Differences also emerge in the specialisation of the two ecosystems: in Italy, digital health predominates, accounting for almost half of new life sciences companies in 2025, whilst in France the most significant sector is medtech.

ALL RIGHTS RESERVED ©